Accurate Loan Payoff Calculator™

Introduction to Loan Payoff Calculation

Payoff Calculator tracks payment amounts on the date paid. Calculate penny-perfect loan balance.

- Allows for missed payments

- Allows for extra payments

- Allows for interest rate changes

- Add fees or charges if needed.

- Export schedule to Excel/XLSX and Word/DOCX files

A perfect calculator for seller financing transactions.

What is a loan payoff amount?

The loan payoff amount is the unpaid principal balance plus all unpaid accrued interest as of a specific date. The borrower must pay this amount on that date to fully repay the loan.

What is a loan payoff calculator?

A loan payoff calculator tracks individual payments on their actual payment dates. It includes overpayments and underpayments to calculate the current loan balance or the final payoff amount.

What is seller financing?

Seller financing, also known as owner financing, is a financing arrangement in which the asset seller—typically the property owner—provides the loan directly to the buyer. The buyer makes payments to the seller, usually after making a down payment.

What is an owner financing calculator?

An owner financing calculator allows the seller or buyer to calculate the current loan balance. It tracks each payment on the actual date it was made, including overpayments and underpayments.

The Accurate Loan Payoff Calculator helps users manage an owner financing agreement or determine the correct loan payoff amount. You can watch the tutorial videos or follow the written instructions below…

Accurate Loan Payoff and Owner Financing Calculator

To set your preferred currency and date format, click the “$ : MM/DD/YYYY” link in the lower-right corner of any calculator.

Information

This calculator helps you calculate the loan payoff amount. It supports on-time, late, missed, and extra payments. It also supports changes to payment amounts and interest rates.

- The Accurate Loan Payoff Calculator is designed for users who need one or more of the following tools:

- loan repayment calculator

- mortgage payoff calculator

- student loan repayment calculator

- home loan repayment calculator

- car loan repayment calculator

- debt payoff calculator

- debt repayment calculator

- early loan payoff calculator

We recommend that all users complete the more detailed first tutorial to understand the calculator’s key concepts and settings.

Owner Financing

Step-by-Step Tutorial — Tutorial 25

Watch on YouTube

To calculate a loan or mortgage balance and to record payments as you receive them, follow these steps:

- Set “Schedule Type” to “Loan”.

- Or click the button to remove any previous entries.

- Click .

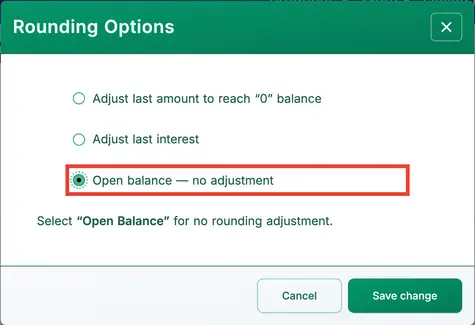

- Set “Rounding” to Open balance — no adjustment.

- This setting allows you to enter individual payments. See Fig. 1.

- Other rounding options will automatically adjust the final payment to bring the loan balance to zero.

- Set “Rounding” to Open balance — no adjustment.

- Click .

- Set the “Days Per Year” option to “360 Days Per Year”.

- In the header section, apply the following settings:

- For “Calculate Method”, select “Normal”.

- Set “Initial Compounding” to “Monthly”.

- Enter 5.25 for the “Initial Interest Rate”.

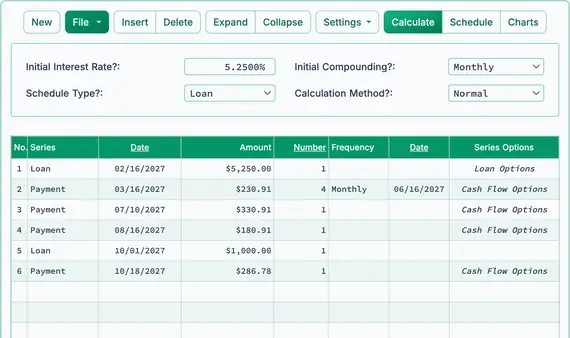

- In row 1 of the cash flow input area, create a “Loan” series:

- Set the “Date” to February 16.

- Set the “Amount” to 5,250.00.

- Set the Number (of Periods) to 1.

- Note: When the number of periods is 1, the calculator does not allow you to set a frequency. If you enter a frequency, it is cleared when you leave the row.

- The next step is usually to calculate the regular periodic payment if it has not already been determined. In this example, assume the payment amount is not yet known. If the payment has already been set, skip to Step 8.

- The borrower agrees to repay the loan in 24 equal monthly payments. What is the required payment amount?

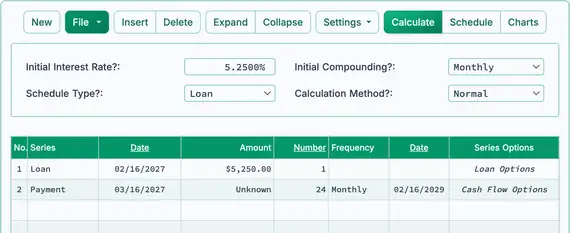

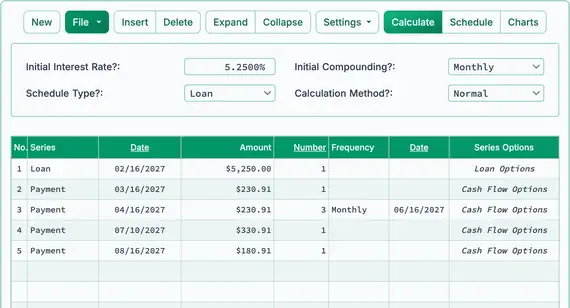

- In the second row, enter the known payment details:

- Set the series to “Payment”.

- Leave the “Date” as March 16.

- In the “Amount” column, type U (for “Unknown”). See Fig. 2.

- Set the number of periods to 24.

- Set the frequency to “Monthly”. (The “End Date” will automatically be February 16.)

- Your screen should now look like this:

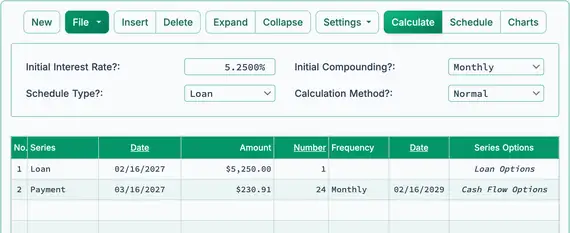

- Click the button.

- The expected periodic payment is $230.91. See Fig. 3.

- You may now begin recording payments as they are received. Because the payment amount was calculated using a schedule with 24 payments, update row 2:

- The first payment is received on time. Click row 2.

- Select “Payment” for the series.

- Leave the date set to March 16.

- In the “Amount” column, enter $230.91.

- Enter 1 for Number (of Periods) to record one payment.

- Assume that the next three payments were also received on time and in the correct amount, but you entered them later. You can enter them now as follows:

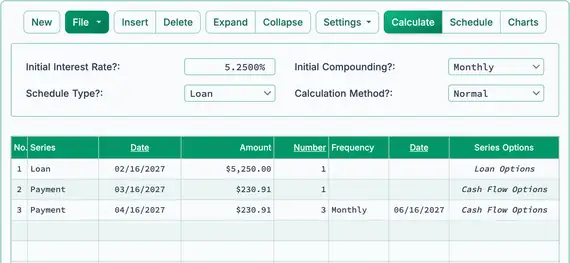

- Click row 3.

- Select “Payment” for the series.

- Set the date to April 16.

- In the “Amount” column, enter $230.91.

- Enter 3 for Number (of Periods).

- Your screen should now look like this. See Fig. 4:

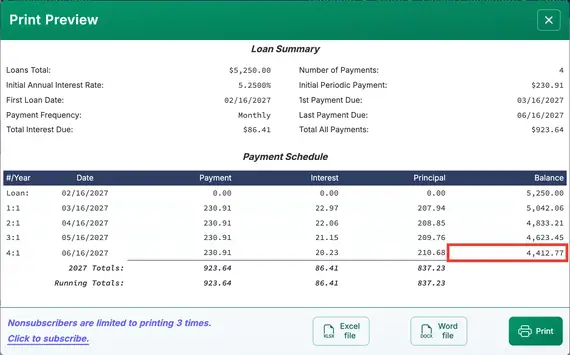

- So far, all payments have been received in the correct amount and on the scheduled due dates. Next, check the loan payoff amount after these four payments:

- Click the button.

- As of June 16, after the payment, the payoff amount is $4,412.77. See Fig. 5.

- The borrower makes the fifth payment early and includes an extra $100.00.

- Record the early payment with the extra amount:

- Click row 4 and set the series to “Payment”.

- Set the date to July 10.

- Set the amount to $330.91. (This includes the extra $100.00.)

- Set the Number (of Periods) to 1.

- The next payment is not made in full, and the borrower is now behind on the payment schedule.

- Record a missed payment followed by a partial payment:

- Click row 5 and set the series to “Payment”.

- Set the date to September 16.

- Set the amount to $180.91.

- Set the Number (of Periods) to 1.

- After four regular payments, one early payment with an extra $100.00, and one payment that is $50.00 short, your cash flow data screen should look like this. See Fig. 6:

- Note: You do not need to enter 0.00 for a missed payment. However, entering it may help with recordkeeping. It explicitly shows the missed payment and causes the calculator to compute the balance as of that payment’s due date.

- Note: Interest is being calculated through August 16 and added to the loan balance.

- The borrower needs additional funds. You approve an additional loan and add it to the existing loan balance.

- Add an additional loan:

- Click the empty row after the last payment. This is row 6.

- Select “Loan” for the series. See Fig. 7.

- Enter October 1 in the Date column. This is the date the funds become available.

- In the “Amount” column, enter the new loan amount: $1,000.00.

- Enter 1 for Number (of Periods) (a single loan disbursement).

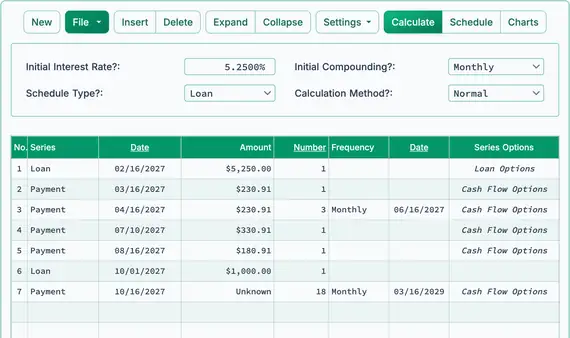

- Because a new loan amount has been added, you will now calculate a new payment. The borrower has agreed to repay the full balance in 18 additional monthly payments.

- Adjust the payment amount based on the new loan:

- Click the empty row following the newly entered loan.

- Select “Payment” for the series.

- Set the Date to October 16. Monthly payments will continue on the 16th of each month.

- In the “Amount” column, type U for “Unknown”.

- Enter 18 for Number (of Periods).

- Set the frequency to “Monthly”.

- If you have been following the tutorial, your screen should now look like this:

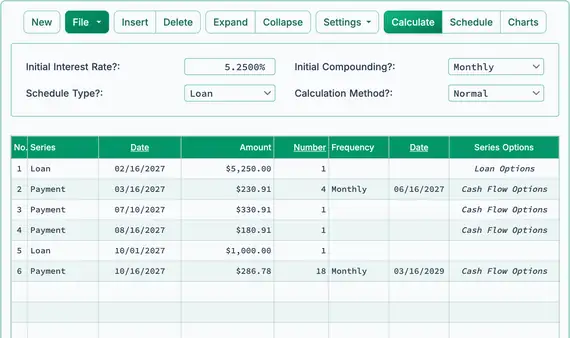

- Click the button.

- The new monthly payment will be $286.78. See Fig. 8.

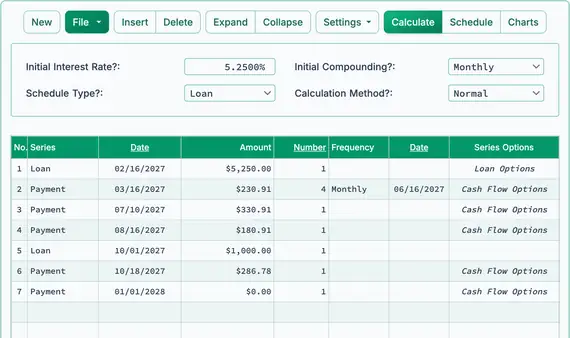

- The borrower makes a full payment but two days late:

- Edit the payment in row 7.

- Leave Series set to “Payment”.

- Change the Date to October 18.

- Leave the Amount set to $286.78 (full payment).

- Change the Number (of Periods) from 18 to 1 (only one payment is being recorded).

- Continue entering payments (and loan advances) as they are received until the loan is fully repaid. You may enter a payment of $0.00 on any date to calculate the loan balance as of that date. See Fig. 10.

- Calculate the unpaid principal balance as of any date:

- Assume no payments are made after October 18:

- Leave Series set to “Payment”.

- Change the Date to January 1.

- Set the Amount to $0.00 (no payment is made). See Fig. 10.

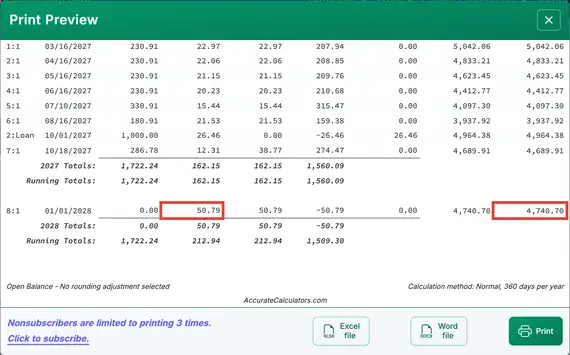

- Click the button. The row for January 1 will display the loan balance, including interest accrued since the October 18 payment. See Fig. 11.

- Calculate the loan’s payoff amount as of any date:

- Repeat the steps from step 17, but set the Amount on January 1 to “Unknown”.

- Change the rounding option to “Adjust last amount to reach a ”0“ balance”.

- The calculator will determine the payoff amount. The schedule will show a final balance of $0.00.

- The calculated payoff amount will match the balance shown in step 17, adjusted for rounding.

- You can display the same loan in two ways:

- Follow the steps in step 17 to view the balance as of January 1.

- Follow the steps in step 18 to calculate the full payoff amount and confirm that the balance is zero.

If you have any questions about the Accurate Loan Payoff Calculator, you may leave them in the comments section below.

TValue is a trademark of TimeValue Software.

Kelsey says:

Correction, first entry was correct. Subsequent entries are off.

Bank:

Date Balance Payment Principal Interest

11/1/2019$123,785.00

12/10/2019$122,480.61$2,164.10 $1,304.39 $859.71

1/6/2020 $119,823.08$3,246.15 $2,657.53 $588.62

3/16/2020$119,812.68$1,500.00 $10.40 $1,489.60

5/4/2020 $119,355.31$1,500.00 $457.37 $1,042.63

6/8/2020 $118,597.21$1,500.00 $758.10 $741.90

7/1/2020 $117,581.64$1,500.00 $1,015.57 $484.43

7/31/2020$116,708.10$1,500.00 $873.54 $626.46

8/31/2020$115,850.63$1,500.00 $857.47 $642.53

10/1/2020$114,988.45$1,500.00 $862.18 $637.82

10/30/2020$114,080.67$1,500.00 $907.78 $592.22

11/30/2020$113,208.73$1,500.00 $871.94 $628.06

1/13/2021$112,594.03$1,500.00 $614.70 $885.30

2/1/2021 $111,475.00$1,500.00 $1,119.03 $380.97

3/3/2021 $110,570.55$1,500.00 $904.45 $595.55

Calculator:

Date Payment Interest Principal Interest

11/01/20190.00 0.00 0.00 123,785.00

1:112/10/20192,164.10859.711,304.39122,480.61

2:101/06/20203,246.15588.912,657.24119,823.37

3:103/16/20201,500.001,493.696.31 119,817.06

4:105/04/20201,500.001,045.53454.47119,362.59

5:106/08/20201,500.00743.97756.03118,606.56

6:107/01/20201,500.00485.801,014.20117,592.36

7:107/31/20201,500.00628.23871.77116,720.59

8:108/31/20201,500.00644.36855.64115,864.95

9:110/01/20201,500.00639.64860.36115,004.59

10:110/30/20201,500.00593.93906.07114,098.52

11:111/30/20201,500.00629.89870.11113,228.41

12:201/13/20211,500.00887.21612.79112,615.62

13:202/01/20211,500.00381.041,118.96111,496.66

14:203/03/20211,500.00595.67904.33110,592.33

Karl says:

Glad you like the calculators.

The interest calculation goes out, as you pointed out, with the second payment. Once there’s a discrepancy, the 2 schedules will never match. This is because, interest is calculated on the balance, and the balance do not agree after the first payment.

Either, the bank has made an error in their calculation, or they are not calculating the interest as you describe.

Here’s the math behind the interest accrued as of the 2nd payment:

Balance – 122,480.61

Rate – 6.5% or 0.065/365 = 0.0001780 daily rate

Dec 10 – Jan. 6 is 27 days.

Thus 27 * 0.0001780 * 122,480.61 = 588.914 = $588.91

Which is the number the calculator calculates for interest with the 01/06/2020 payment.

I did look at the bank’s calculation, but could not figure out how they are coming up with 588.62. Are you sure they are using a rate based on days and not a monthly rate, i.e. 6.5%/12? I did not attempt that calculation because I did not know how they would account for the odd days.

The bank should be able to document their math. I would love to hear what they say.

Kelsey says:

I have discovered the issue. The problem occurs during a pay period that spans a year change that includes a regular year and a leap year. Part of the days should be calculated at 365 and part at 366. For example the payment made on 1/6/20 should be calculated as follows:

12/10-12/31

0.065/365*22 days*122480.61=479.86

PLUS

1/1-1/5

0.065/366*5 days*122480.61=108.76

Add those two together and you get $588.62. This would not be relevant if all payments made in the new year were always made on 1/1 but mine never are. If you make this correction, all the subsequent calculations are correct (except a few rounded pennies here and there) till you get the end of the leap year and have to make the correction again and then when more leap years occur. Not sure if this is normal practice and if your calculator would need the correction.

Karl says:

Thanks, Kelsey. I’ll take a look. I had thought of this possibility when replied, but I had done the math and came up with $588.56 somehow. I must have had a number transposed somewhere. I wish I had saved my work. 🙁

This will be a significant update. I’ll take a look over the next 30 days.

Concerning whether it’s normal practice, I had not run into it until recently, but some lenders do follow a 366 day leap year convention when the period spans a non-leap year/leap year.

Karl says:

Kelsey, I posted today an update to the calculator the supports 366-day years. I’ll send you a file that you drag and drop to load your example. The final balance differs from you bank example by one cent. If I trace the one cent back to where there is the first difference, I see it here:

Your example has $741.90 for the interest on June 8, 2020. However, this is the arithmetic:

prior period’s balance times daily rate 6.5/100/366 times number of days

= 119,355.31 * 0.0001775956 * 35 = 741.8943 or $741.89

Most likely, the bank’s calculation does not maintain the same degree of precision in the rate as this calculator does.

Bobby says:

Am I correct in assuming that the interest is calculated from the “principal balance” and not the “balance?” And, it seems that if a debtor misses a few payments and then pays some irregular partial payments, the payments are applied to interest first, and if additional interest is still due, it adds the interest to the principal balance. Is there a way to set up the calculator to calculate interest off the principal balance and apply payments to interest first (without ever adding any interest to the principal balance)? I assumed that this would have been the result when I selected the “simple” interest option. Thanks.

Karl says:

Assuming the calculation method is set to "Normal", interest is calculated on the loan balance as of some date based on the number of periods since the last interest calculation, added to the loan balance and then the payment is deducted. The loan balance is the loan balance. That is, if there is unpaid interest, then the loan balance will also include that interest.

It sounds to me as if you want to calculate interest on the principal balance only. That is, if there is unpaid interest, it will not be included in the next interest calculation. This calculation supports that. Set calculation method to "US Rule." US Rule means "no interest on interest."

If this is not what you need, please let me know. Or if it’s what you want, you can let me know that too. 🙂

Adam says:

(sorry if this appears twice)… I couldn’t find my other comment

I am trying to calculate daily interest based on US rule. I am getting error message “Error: Daily, continuous or no (“none”) compounding cannot be used with US Rule loans.”

Commercial loan says “total amount is calculated daily based on actual days and a 360 day year, at an interest rate of 8.75% per annum”

Based on some documents provided by lender – It appears that lender is calculating interest off of the amount of principal balance that remains unpaid. Interest is NOT added to principal. Late Fees are NOT added to principal. Other charges/costs ARE added to principal balance.

It appears interest is compounded daily

There have been late payments, and some months with multiple payments.

Trying to calculate.

Any help would be appreciated.

Karl says:

The U.S. Rule option means that interest will not be calculated on interest.

Daily compounding means that interest is calculated on the prior day’s interest.

Thus these two options, as the informational message indicates are mutually exclusive.

Since you want the interest basis to be daily, set the compounding to "Exact/Simple."

Mark WOELFLE says:

I have a 30 yr. loan with 20 years left on it ( $130,000 balance) at 3.875%. Thinking of going to either 15 yr. loan at 2.00% with no points or just paying down the principal 100.00 or 200.00 dollars each month to eliminate loan processing fees. I cant find a calculator that will show me the saving if i just pay down the principal. Current payment is 754.73 each month.what would be the more logical way to go in most cases. thanks

Karl says:

One way you can approach this is to use this calculator and create 2 different amortization schedules – one for each scenario that you describe. Then look at the end of the schedule and compare the total interest amounts paid under each paydown method.

Peggy says:

The Ultimate Loan Payoff Calculator seems to be exactly what I need! I don’t feel like my bank is properly calculating my monthly interest and was looking for a way to calculate interest based on the actual date of payment.

I don’t see how I can purchase and download this calculator. Please advise.

Thanks !!

Karl says:

The UFC will do what you want, as you have apparently discovered.

If you would rather have a Windows program with similar features, than please look at C-Value!. However, the online calculator is a bit more up to date, and unless you have a significant reason for wanting a Windows program rather than using the online calculator, I can’t think of why you would want to pay the $50 for C-Value!.

Richard says:

Great calculator Karl,

I hadn’t noticed any discussion regarding this. Can the calculator track late charges and their payments?

Thanks in advance for your response,

Richard

Karl says:

Thank you!

Yes, under series, the "Fee"e; can be used for late charges.

And payments are payments. If you want to track a payment to a late charge then add a comment to the payment, under "Cash Flow Options."

Does that work for you?

Robert Romero says:

If there is a change in Interest Rate due to a payment default can that be done here.

Robert Romero says:

Regarding The Rate Change, I was able to find it. I should have waited to ask until after playing with it a bit. What a great tool. I have been doing this semi-manually using an amortization calculator but it was so much work recalculating for the differing payments I was receiving.

Thanks so Much!

Karl says:

You’re quite welcome. And very glad to hear that using the calculator is better than doing the calculation "semi-manually." 🙂

James A Fivian says:

I have been using your tutorial to enter data on a personal loan I am Holding. I am unaware of how to download the program to my Mac. At this point I enter data and minimize the tutorial until the next payment is made. In the interim I must be very careful when using Safari or I will lose everything. That has happened frequently.

I see that recently you have notified us that the number of printings will be restricted for non registered users. How do I become a registered user? New tricks are hard on old dogs. Thanks

Karl says:

You can’t download it to your Mac. The calculator is a web calculator.

But you do not need to be careful using Safari either. Shut your computer off if you want to.

What you need to do first is click on the "File" then "Save as…." and this will give you the opportunity so save the data to a file on your disk that you can then open with the "File", "Open" menu choice.

Also, this calculator is not limited in anyway (presently).

Kathy says:

Hi Karl,

Is there a way to add a 5% late charge to delinquent installment payments in addition to the interest?

Thanks for your assistance.

Karl says:

Hi Kathy,

In the dropdown list under “Series,” one of the choices is “Fees.” Fees can be used to enter any charges that get added to the loan. The user can’t enter percentages, however. You’ll need to do the arithmetic and enter the amount.