Accurate Loan Payoff Calculator™

Introduction to Loan Payoff Calculation

Payoff Calculator tracks payment amounts on the date paid. Calculate penny-perfect loan balance.

- Allows for missed payments

- Allows for extra payments

- Allows for interest rate changes

- Add fees or charges if needed.

- Export schedule to Excel/XLSX and Word/DOCX files

A perfect calculator for seller financing transactions.

What is a loan payoff amount?

The loan payoff amount is the unpaid principal balance plus all unpaid accrued interest as of a specific date. The borrower must pay this amount on that date to fully repay the loan.

What is a loan payoff calculator?

A loan payoff calculator tracks individual payments on their actual payment dates. It includes overpayments and underpayments to calculate the current loan balance or the final payoff amount.

What is seller financing?

Seller financing, also known as owner financing, is a financing arrangement in which the asset seller—typically the property owner—provides the loan directly to the buyer. The buyer makes payments to the seller, usually after making a down payment.

What is an owner financing calculator?

An owner financing calculator allows the seller or buyer to calculate the current loan balance. It tracks each payment on the actual date it was made, including overpayments and underpayments.

The Accurate Loan Payoff Calculator helps users manage an owner financing agreement or determine the correct loan payoff amount. You can watch the tutorial videos or follow the written instructions below…

Accurate Loan Payoff and Owner Financing Calculator

To set your preferred currency and date format, click the “$ : MM/DD/YYYY” link in the lower-right corner of any calculator.

Information

This calculator helps you calculate the loan payoff amount. It supports on-time, late, missed, and extra payments. It also supports changes to payment amounts and interest rates.

- The Accurate Loan Payoff Calculator is designed for users who need one or more of the following tools:

- loan repayment calculator

- mortgage payoff calculator

- student loan repayment calculator

- home loan repayment calculator

- car loan repayment calculator

- debt payoff calculator

- debt repayment calculator

- early loan payoff calculator

We recommend that all users complete the more detailed first tutorial to understand the calculator’s key concepts and settings.

Owner Financing

Step-by-Step Tutorial — Tutorial 25

(concise version)

Watch on YouTube

Watch on YouTube

To calculate a loan or mortgage balance and to record payments as you receive them, follow these steps:

- Set “Schedule Type” to “Loan”.

- Or click the button to remove any previous entries.

- Click .

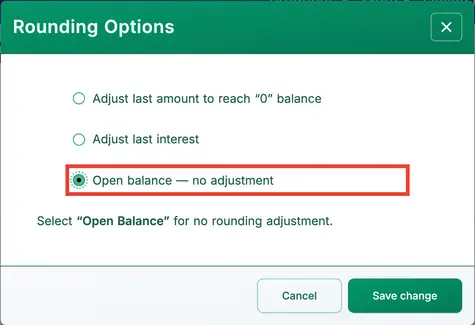

- Set “Rounding” to Open balance — no adjustment.

- This setting allows you to enter individual payments. See Fig. 1.

- Other rounding options will automatically adjust the final payment to bring the loan balance to zero.

- Set “Rounding” to Open balance — no adjustment.

- Click .

- Set the “Days Per Year” option to “360 Days Per Year”.

- In the header section, apply the following settings:

- For “Calculate Method”, select “Normal”.

- Set “Initial Compounding” to “Monthly”.

- Enter 5.25 for the “Initial Interest Rate”.

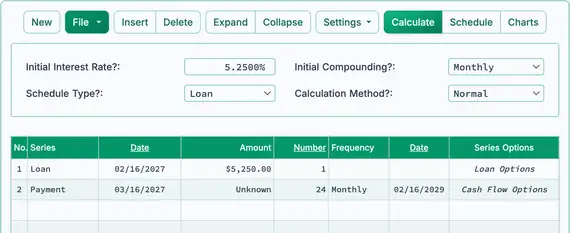

- In row 1 of the cash flow input area, create a “Loan” series:

- Set the “Date” to February 16.

- Set the “Amount” to 5,250.00.

- Set the Number (of Periods) to 1.

- Note: When the number of periods is 1, the calculator does not allow you to set a frequency. If you enter a frequency, it is cleared when you leave the row.

- The next step is usually to calculate the regular periodic payment if it has not already been determined. In this example, assume the payment amount is not yet known. If the payment has already been set, skip to Step 8.

- The borrower agrees to repay the loan in 24 equal monthly payments. What is the required payment amount?

- In the second row, enter the known payment details:

- Set the series to “Payment”.

- Leave the “Date” as March 16.

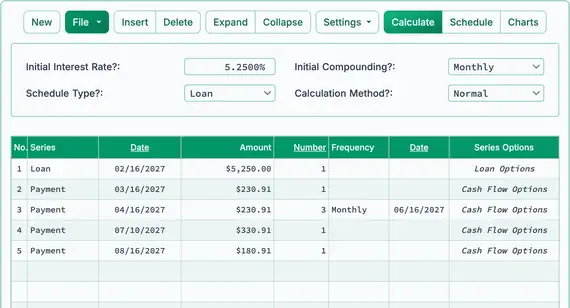

- In the “Amount” column, type U (for “Unknown”). See Fig. 2.

- Set the number of periods to 24.

- Set the frequency to “Monthly”. (The “End Date” will automatically be February 16.)

- Your screen should now look like this:

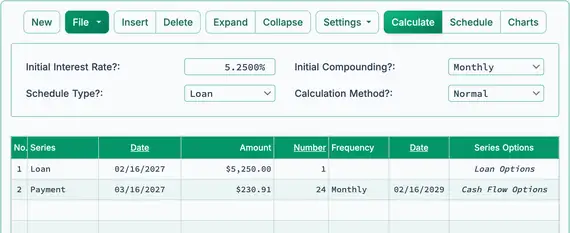

- Click the button.

- The expected periodic payment is $230.91. See Fig. 3.

- You may now begin recording payments as they are received. Because the payment amount was calculated using a schedule with 24 payments, update row 2:

- The first payment is received on time. Click row 2.

- Select “Payment” for the series.

- Leave the date set to March 16.

- In the “Amount” column, enter $230.91.

- Enter 1 for Number (of Periods) to record one payment.

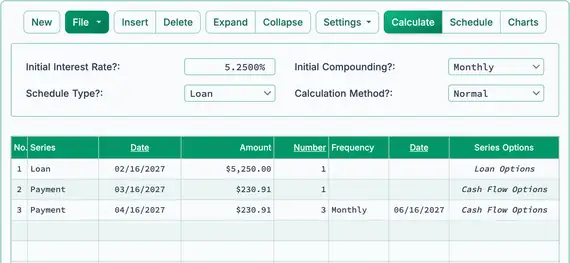

- Assume that the next three payments were also received on time and in the correct amount, but you entered them later. You can enter them now as follows:

- Click row 3.

- Select “Payment” for the series.

- Set the date to April 16.

- In the “Amount” column, enter $230.91.

- Enter 3 for Number (of Periods).

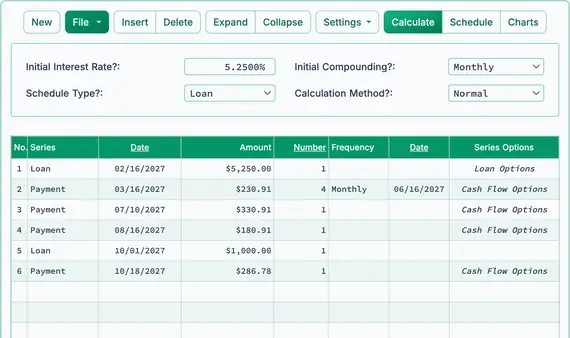

- Your screen should now look like this. See Fig. 4:

- So far, all payments have been received in the correct amount and on the scheduled due dates. Next, check the loan payoff amount after these four payments:

- Click the button.

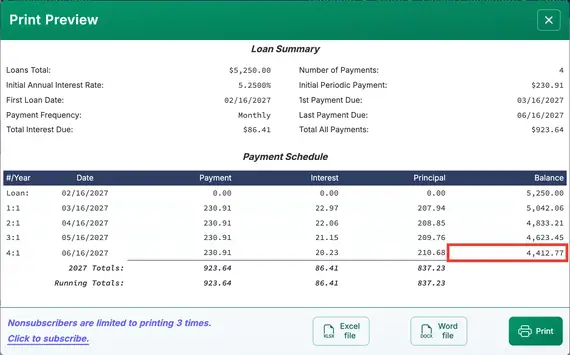

- As of June 16, after the payment, the payoff amount is $4,412.77. See Fig. 5.

- The borrower makes the fifth payment early and includes an extra $100.00.

- Record the early payment with the extra amount:

- Click row 4 and set the series to “Payment”.

- Set the date to July 10.

- Set the amount to $330.91. (This includes the extra $100.00.)

- Set the Number (of Periods) to 1.

- The next payment is not made in full, and the borrower is now behind on the payment schedule.

- Record a missed payment followed by a partial payment:

- Click row 5 and set the series to “Payment”.

- Set the date to September 16.

- Set the amount to $180.91.

- Set the Number (of Periods) to 1.

- After four regular payments, one early payment with an extra $100.00, and one payment that is $50.00 short, your cash flow data screen should look like this. See Fig. 6:

- Note: You do not need to enter 0.00 for a missed payment. However, entering it may help with recordkeeping. It explicitly shows the missed payment and causes the calculator to compute the balance as of that payment’s due date.

- Note: Interest is being calculated through August 16 and added to the loan balance.

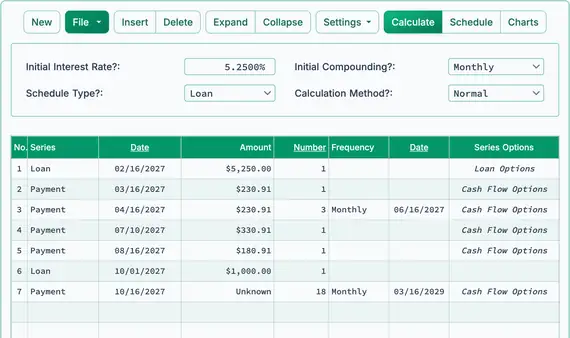

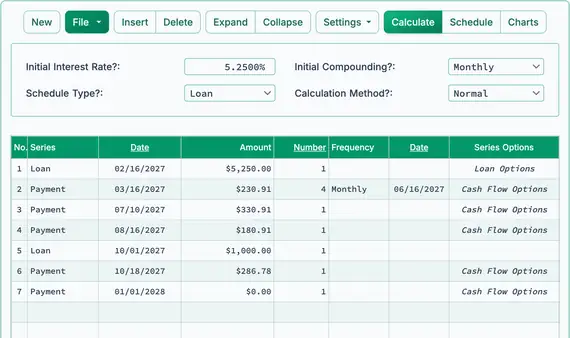

- The borrower needs additional funds. You approve an additional loan and add it to the existing loan balance.

- Add an additional loan:

- Click the empty row after the last payment. This is row 6.

- Select “Loan” for the series. See Fig. 7.

- Enter October 1 in the Date column. This is the date the funds become available.

- In the “Amount” column, enter the new loan amount: $1,000.00.

- Enter 1 for Number (of Periods) (a single loan disbursement).

- Because a new loan amount has been added, you will now calculate a new payment. The borrower has agreed to repay the full balance in 18 additional monthly payments.

- Adjust the payment amount based on the new loan:

- Click the empty row following the newly entered loan.

- Select “Payment” for the series.

- Set the Date to October 16. Monthly payments will continue on the 16th of each month.

- In the “Amount” column, type U for “Unknown”.

- Enter 18 for Number (of Periods).

- Set the frequency to “Monthly”.

- If you have been following the tutorial, your screen should now look like this:

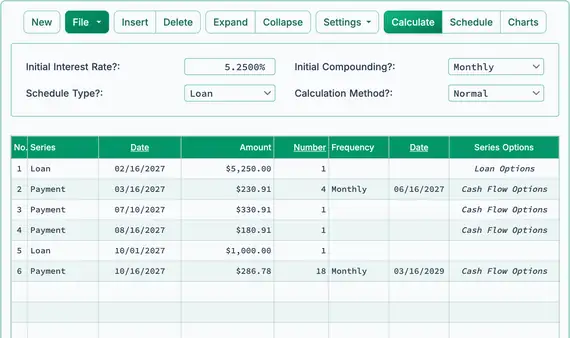

- Click the button.

- The new monthly payment will be $286.78. See Fig. 8.

- The borrower makes a full payment but two days late:

- Edit the payment in row 7.

- Leave Series set to “Payment”.

- Change the Date to October 18.

- Leave the Amount set to $286.78 (full payment).

- Change the Number (of Periods) from 18 to 1 (only one payment is being recorded).

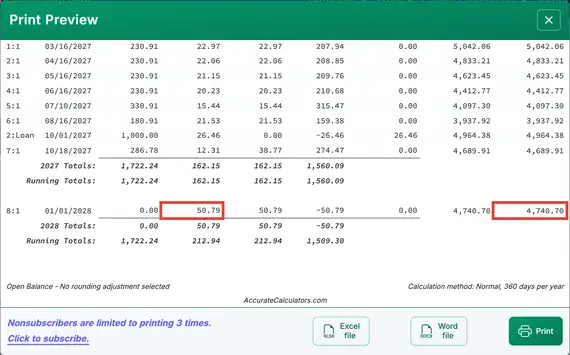

- Continue entering payments (and loan advances) as they are received until the loan is fully repaid. You may enter a payment of $0.00 on any date to calculate the loan balance as of that date. See Fig. 10.

- Calculate the unpaid principal balance as of any date:

- Assume no payments are made after October 18:

- Leave Series set to “Payment”.

- Change the Date to January 1.

- Set the Amount to $0.00 (no payment is made). See Fig. 10.

- Click the button. The row for January 1 will display the loan balance, including interest accrued since the October 18 payment. See Fig. 11.

- Calculate the loan’s payoff amount as of any date:

- Repeat the steps from step 17, but set the Amount on January 1 to “Unknown”.

- Change the rounding option to “Adjust last amount to reach a ”0“ balance”.

- The calculator will determine the payoff amount. The schedule will show a final balance of $0.00.

- The calculated payoff amount will match the balance shown in step 17, adjusted for rounding.

- You can display the same loan in two ways:

- Follow the steps in step 17 to view the balance as of January 1.

- Follow the steps in step 18 to calculate the full payoff amount and confirm that the balance is zero.

If you have any questions about the Accurate Loan Payoff Calculator, you may leave them in the comments section below.

TValue is a trademark of TimeValue Software.

Riley Shannon says:

We have an AM schedule where extra payments are made throughout. Is it possible to allocate an extra payment between interest and principal? Periodically, we want to allocate a specific dollar amount of the extra payment to the accrued interest balance. For example: We have a $4.7M payment; can we allocate $3.9M to principal and $800K to interest? Thanks in advance!

Karl says:

The answer is, "it depends."

If the accrued interest exceeds $800k, then the answer is "Yes," otherwise it is "No."

What you will need to do is is to allocate the $4.7 million across two payments (rows in the calculator) made on the same date.

The first of the two rows should be a "normal" payment, for $800k. Since the normal payment gets allocated to interest and then to principal, this row will cover the $800k you want to allocate to interest.

The second row will be an "XPmt" for $3.9M. This will be allocated to principal only.

Let me know please if this helps.

Riley Shannon says:

Thank you so much!

jrslaw6565.bks@gmail.com says:

Can you add rows to the tables or is it limited to the number of payments you can enter

Karl says:

The "Insert" button will insert an empty row.

You can also go to the next row after the last row with data and enter say 500 in the # column and click expand. This will create 500 rows, prefilled with the dates.

If this isn’t what you mean, tell me what you are trying to do that you can’t do. I’ve never had anyone indicate there are not enough rows already in the table area.

llittleton says:

Loan original date it 9/1/2021. First payment is made 3/9/2022. It is putting in a payment in 2021 that was never made. How do I stop this?

Karl says:

I am assuming that the payment frequency is monthly, and that the payment you are seeing is for the prepaid interest on the loan origination date.

If this is the case, you can click on "Settings", followed by "Interest Options" and in the window that opens, set the interest to "With first".

If this is not what you are seeing, let me know.