Accurate Construction Loan Calculator™

Use this construction loan calculator for multiple, irregular borrows and exact-date interest-only or P&I payments.

- Payments can be regular or irregular

- Print date accurate schedules.

- Supports interest rate changes

- NEW: Export to XLSX/DOCX files

- NEW: YouTube video shows you how to use it.

Suitable for bankers, accountants, attorneys and you!

What is a construction loan?

A construction loan provides short-term financing to cover building costs while a property is being developed. Unlike traditional mortgages, a construction loan is disbursed in multiple phases at predetermined construction milestones, rather than as a single lump sum.

What is a construction loan calculator?

A construction loan calculator tracks multiple loan disbursements issued at irregular intervals, along with any payments made by the borrower. Using these inputs, the calculator determines the outstanding loan balance at any selected date.

How do you use the Accurate Construction Loan Calculator (ACLC)?

This tutorial explains each step in the process. By the end, you will be able to monitor payments and calculate the loan balance as of any chosen date.

How construction loans differ from traditional mortgages

In most cases, lenders do not issue a mortgage on a property that has not yet been built. In these situations, a future homeowner must apply for a home construction loan.

Unlike mortgages, which are funded in a single disbursement, construction loans are issued in multiple draws. The borrower, builder, and lender agree on the total cost of construction and the portion that will be financed. The borrower then receives funds incrementally, as each construction milestone is completed.

This incremental disbursement structure helps reduce risk for the lender and potential cost for the borrower. For example, if the entire loan were issued upfront and the builder defaulted, the borrower would still be responsible for repaying the full amount. By controlling disbursements, the lender protects both parties.

Such issues are uncommon when working with a reputable builder. However, construction loans still help reduce financial risk and limit interest costs.

Why construction loans can save money

The borrower pays interest only on the amounts that have actually been drawn, not on the full loan amount. As new disbursements are made, the outstanding loan balance increases gradually. This helps limit total interest charges.

Although the savings may not always be large, reducing interest expenses is still beneficial. However, construction loans usually have higher interest rates than traditional mortgages. This reflects the additional risk that the lender takes during the construction phase.

More below…

Construction Loan Calculator with multiple loan disbursements

To set your preferred currency and date format, click the “$ : MM/DD/YYYY” link in the lower-right corner of any calculator.

Information

What Are the Two Types of Construction Loans?

- Stand-alone construction — the borrower must apply for a separate mortgage in addition to the construction loan.

- Construction-to-permanent — this loan automatically converts to a mortgage, usually when the local authority issues a certificate of occupancy (CO).

The loan type does not change how the calculation is performed. However, for the borrower, a construction-to-permanent loan is often more favorable because it removes the risk that a mortgage will not be approved after construction is complete.

However, a construction-to-permanent loan agreement may require the borrower to convert the loan to a mortgage with the same lender. If the borrower chooses another lender, a penalty may apply. This condition may be a disadvantage if interest rates fall during construction, because the borrower may be locked into a higher mortgage rate.

Plus Two Amortization Methods

Once the lender begins disbursing funds to the builder, the borrower is generally required to begin making regular payments. This applies whether the loan is stand-alone or construction-to-permanent.

There are two standard methods for calculating payments:

- The payment includes both principal and interest (P&I).

- The payment includes interest only.

The Accurate Construction Loan Calculator supports both options and can generate a complete amortization schedule.

This calculator works equally well for both home construction loans and commercial construction loans.

Step-by-step instructions follow. Because interest-only construction loans are more common, this tutorial covers that option first.

All users should first complete the more detailed initial tutorial to understand the basic concepts and settings of the Ultimate Financial Calculator (UFC).

A Step-by-Step Tutorial

Calculate a Construction Loan with Multiple Loan Advances — Tutorial 11

Watch on YouTube

Interest-Only Construction Loan

To create a construction loan amortization schedule with interest-only payments, follow these steps:

- Set Schedule Type to Loan.

- Or click to clear any existing entries.

- Click , and set Rounding to Adjust the last amount to reach 0 balance.

- In the header section, apply the following settings:

- For Calculation Method, select U.S. Rule.

- This method prevents the calculator from charging interest on previously accrued but unpaid interest when a new loan amount is disbursed. To compare results, you may switch to Normal.

- Set Initial Compounding to Exact/Simple.

- Enter 5.5 for the Initial Interest Rate.

- For Calculation Method, select U.S. Rule.

- In row 1 of the cash-flow input area, create a Loan series:

- Set the Date to May 16.

- Set the Amount to 75,000.00.

- Set the Number (of Periods) to 1.

- Note: When the number of periods is 1, the frequency cannot be set. If a frequency is entered, the calculator will remove it when you leave the row.

- Go to the second row of the cash-flow input area. Create the anticipated payment schedule:

- Select Payment for the Series.

- Set the Date to July 1.

- Set the Amount to Unknown by typing U.

- Set Number (of Periods) to 5.

- This example assumes construction will last five months, with one payment due on the first of each month.

- You can change this value later if needed.

- Press Tab to move to the Frequency field. Select Monthly.

- The calculator will automatically compute the End Date.

- Click . Select Interest-Only, then click Activate “Interest-Only” payment amount for currently selected series. Click Save Changes.

- If Number (of Periods) is set to 1, the button may not appear. Temporarily change it to 2 to access the options, then return it to 1 if required.

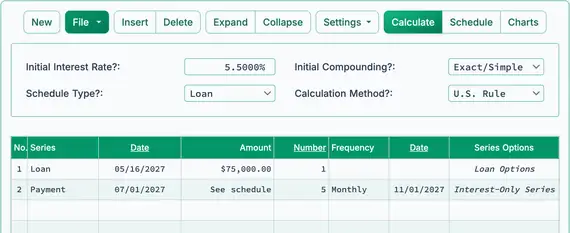

- Your calculator should now look like this (Fig. 1):

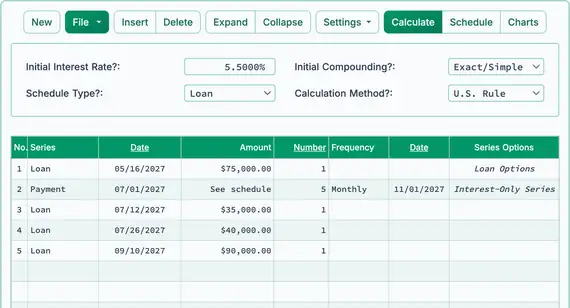

- Construction is ongoing. Enter three additional loan disbursements.

- In row 3 of the cash-flow input area, create a Loan event:

- Set the Date to July 12.

- Set the Amount to $35,000.00.

- Set the Number (of Periods) to 1.

- In row 4, create another Loan series:

- Set the Date to July 26.

- Set the Amount to $40,000.00.

- Set the Number (of Periods) to 1.

- In row 5, create a third Loan series:

- Set the Date to Sept. 10.

- Set the Amount to $90,000.00.

- Set the Number (of Periods) to 1.

- Your screen should now appear like this (Fig. 2):

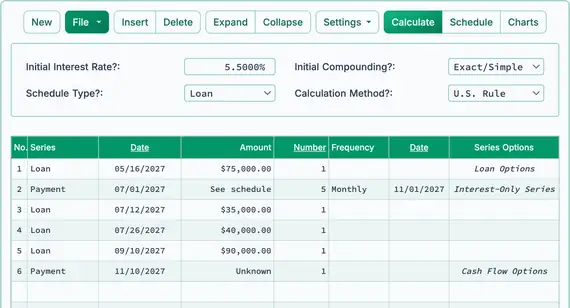

- In this example, we expect to receive the certificate of occupancy and convert the construction loan to a mortgage on November 10. At that time, calculate the final loan balance, including accrued interest.

- In row 6, select Payment for the Series:

- Set the Date to Nov. 10.

- Type U to set the Amount to Unknown.

- Set Number (of Periods) to 1. See Fig. 3.

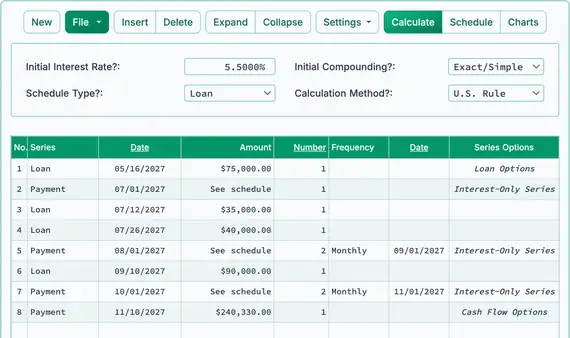

- Now calculate the final payment due. See Fig. 4.

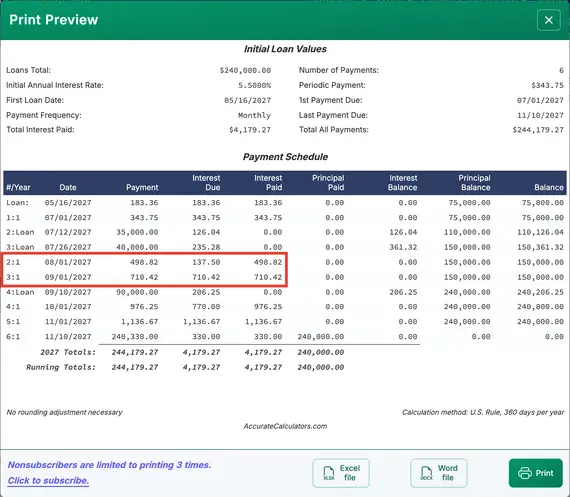

($240,000 principal plus $330.00 accrued interest)

- After calculation, row 6 shows the loan balance due as of the selected date.

- To update the calculation, change the payment date. You can also set the amount to Unknown and recalculate. The final payment will adjust based on the new date.

- Periodic interest payments will also update as additional disbursements occur. Review the amortization schedule to see full details.

- If the borrower misses a scheduled payment, click and update the affected payment date.

- If the construction project runs longer than planned:

- Adjust the projected number of payments, or

- If rows have already been expanded and edited, insert a new, single interest-only payment row.

- Click to view the detailed interest-only amortization schedule. See Fig. 5.

Construction Loan with Principal and Interest Payments

To create a construction loan amortization schedule with P&I (principal and interest) payments, follow these steps:

- Set Schedule Type to Loan.

- Or click to clear any previous entries.

- Click , and set Rounding to Adjust the last amount to reach 0 balance.

- In the header section, apply the following settings:

- For Calculation Method, select Normal.

- Set Initial Compounding to Monthly.

- Enter 7.25 for