Calculating How to Pay for College

To set your preferred currency and date format, click the “$ : MM/DD/YYYY” link in the lower right corner of any calculator.

A Step-by-Step Tutorial

Tutorial 18

Paying for a college education requires careful planning.

The most common question is: “How much do I need to save to pay for college?” To answer this accurately, you need a calculator that can handle multiple cash flows—a series of investments followed by a series of withdrawals. (College payments are usually due at the start of each semester over a 3.5-year period.) The Ultimate Financial Calculator is well suited for this type of planning.

All users should work through the more detailed first tutorial to understand the Ultimate Financial Calculator’s (UFC) basic concepts and settings.

Assumption: For this example, we assume a year of college will cost $60,000. This is a rough, pre-inflation estimate for a four-year private college, based on CollegeData.com (2022):

In its 2022 report, Trends in College Pricing and Student Aid, the College Board reports that a moderate college budget for an in-state student attending a four-year public college in 2022–2023 averages $27,940. For out-of-state students at public colleges, the average is $45,240. For private colleges, the average is $57,570.

The purpose of this tutorial is not to predict future tuition costs. The goal is to demonstrate how to plan and save for those costs. You can change the assumptions to match your own expectations.

See below for options to adjust for inflation.

How long do you have to invest for college? This tutorial includes two examples.

Example 1

To create a savings schedule with an unknown investment amount followed by a series of withdrawals, follow these steps:

- Set Schedule Type to Savings.

- Alternatively, click the button to clear any previous entries.

- The top row of the grid may not be empty.

- Click , then select . Set “Rounding” to Open balance — no adjustment.

- In the header section, make the following settings:

- For Calculation Method, select Normal.

- Set Initial Compounding to Daily.

- Enter 5.0 for Initial Interest Rate.

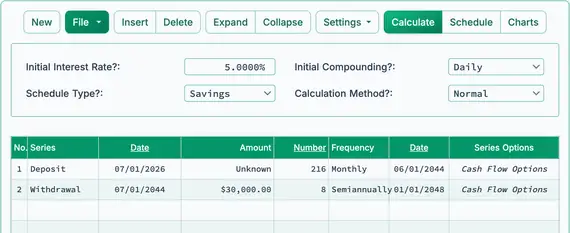

- In row 1 of the cash‑flow input area, create a “Deposit” series.

- Set the “Date” to July 1, 2026.

- Set the “Amount” to Unknown by typing U.

- Set the Number (of Periods) to 258.

- This represents 21.5 years.

- Assumes the student is born in the first half of 2026.

- Set the “Frequency” to Monthly.

- The calculated “End Date” will be December 1, 2047.

- Monthly investments stop when the student turns 21.5 years old.

- Click row 2 of the cash‑flow input area. Set the “Series” to Withdrawal.

- Set the “Date” to July 1, 2044.

- Type all 8 digits to enter the date quickly.

- Note the overlapping dates: withdrawals begin before the investments end.

- Set the “Amount” to 30,000.00.

- This is the estimated semester expense.

- Use the Tab key to move to Number (of Periods). Set it to 8.

- Set the “Frequency” to Semiannually.

- This assumes 8 semester payments spaced 6 months apart.

- Payments start in the year the student turns 18.

- Set the “Date” to July 1, 2044.

- Before calculating, your screen will look like this (Fig. 1):

- This setup illustrates a complex cash flow:

- The first withdrawal occurs about 3.5 years before the last investment. (Compare the “End Date” in row 1 to the “Date” in row 2.)

- The investment frequency is monthly; the withdrawal frequency is semiannual.

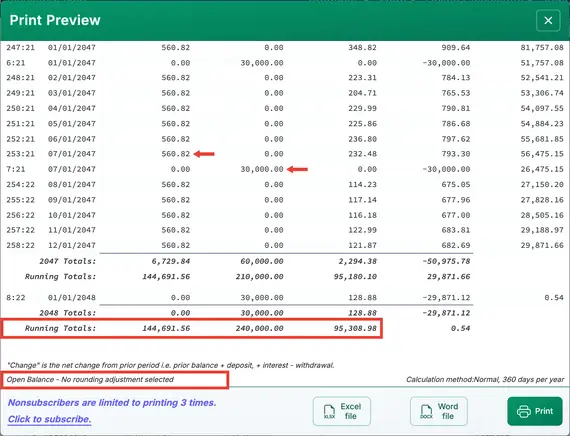

- Click . The result is $560.82. See Fig. 2.

- Invest $560 monthly for 21.5 years at 5.0% to cover college expenses.

- Click .

- The schedule clearly shows monthly investments continuing after withdrawals begin.

(Monthly investments continue after tuition payments start.)

Example 2

This example compares the previous approach to a more traditional savings plan. It calculates how much you need to invest each month, using the same assumptions, with one key change: the full amount for four years of college is available at the beginning of the student’s freshman year.

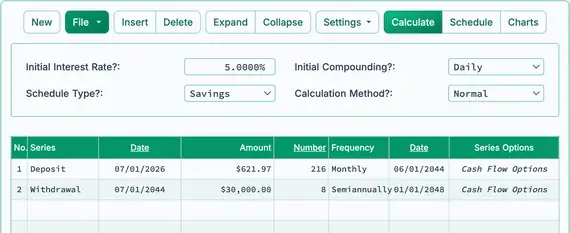

- Edit row 1 of the “Deposit” series.

- Set the “Amount” to Unknown by typing U.

- Set the Number (of Periods) to 216. See Fig. 4.

- Investments stop when the student turns 18 years old.

- This still assumes the student is born in the first half of 2026.

- No changes are needed for the “Withdrawal” series.

- Before the calculation, your screen will look like this (Fig. 4):

- This example has a simpler cash flow:

- Withdrawals begin after the final investment date.

- Investments occur monthly; withdrawals occur semiannually.

- Click . The result is $621.97. See Fig. 5.

- As an alternative, invest $621 monthly for 18 years at 5.0% to fully cover college expenses.

- Click .

- Monthly investments stop before tuition withdrawals begin.

(Monthly investments stop before tuition payments start.)

Return to the Ultimate Financial Calculator.