Calculating the Present Value of a Fixed Principal Loan

To set your preferred currency and date format, click the “$ : MM/DD/YYYY” link in the lower right corner of any calculator.

A Step-by-Step Tutorial

Tutorial 21

Unlike “normal” loans that have a fixed payment, fixed principal loans have declining payment amounts.

With a normal loan, the portion of each payment that is applied to the principal increases over time. This happens as the interest portion decreases. The interest amount declines because the loan balance decreases after each payment.

With fixed principal loans, the portion applied to principal remains the same in every period. However, since the loan balance declines, the interest due also decreases. As a result, each payment includes the fixed principal amount and a smaller interest amount, causing the total payment to decline over time.

Calculating the present value of a fixed principal loan can be time-consuming because payment amounts change. Normally, each payment must be entered individually. However, with the Ultimate Financial Calculator, this is not necessary. This tutorial shows how to discount any cash flow using analytical methods.

All users should review the more detailed first tutorial to understand the basic settings and concepts of the Ultimate Financial Calculator (UFC).

To calculate the present value of a fixed principal loan that includes two interest-only payments, follow these steps:

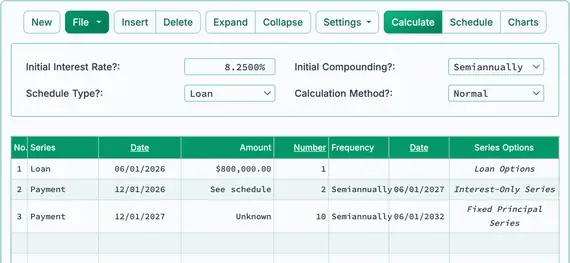

- Set Schedule Type to “Loan”.

- Or click the button to clear any previous entries.

- Set Rounding to “Adjust last amount to reach “0” balance”.

Click , then select . - Set 365 Days Per Year.

Click , then select . - In the header section, apply the following settings:

- Set Calculation Method to “Normal”.

- Set Initial Compounding to “Semiannually”.

- Enter 8.25 for Initial Interest Rate.

- In row one of the cash flow input area, create a “Loan” series:

- Set the Date to June 1, 2026.

- Set the Amount to 800,000.00.

- Set the Number (of Periods) to 1.

- Note: Since the number of periods is 1, you cannot set a frequency. If a frequency is selected, it will be cleared when you leave the row.

- In row two, create a “Payment” series:

- Set the Date to December 1, 2026.

- Set Number (of Periods) to 2.

- Set Frequency to “Semiannually”.

- Click the second row’s and activate an “Interest-Only” series.

- See the related interest-only payment tutorial.

- Number (of Periods) must be greater than 1 to access the link.

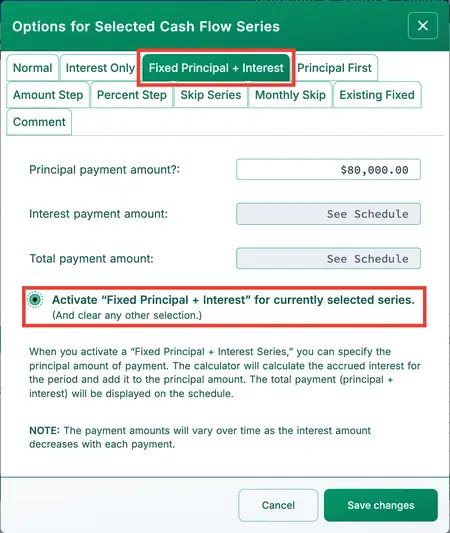

- In row three, create a “Fixed Principal + Interest” Payment series.

- Set the Date to December 1, 2027.

- Set the Amount to Unknown by typing U.

- Set Number (of Periods) to 10.

- Set Frequency to “Semiannually”.

- Click and activate a “Fixed Principal + Interest” series.

- Number (of Periods) must be greater than 1 to access the link.

- Before calculating, your screen will look like this:

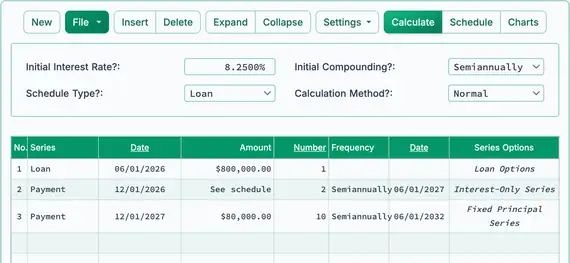

- Calculate the unknown. The result is $80,000.00.

- This amount is the fixed principal value. It does not include interest.

- View the schedule to see each declining payment. Each payment includes interest.

- Up until this point, you have been using the calculator to build a moderately complex fixed principal loan schedule. If you are an investor evaluating a loan purchase, you must also determine the present value of the future cash flow as of your investment date. This is easy to calculate. Begin by entering your discount rate, which is the rate of return you expect to earn from the investment.

- Click , then select .

- Set Discount Rate to 6.5.

- Set As of Date to September 30, 2026.

- Select “Include present value (PV) on schedule...”.

- Click to close.

- Click the button.

- As of September 30, 2026, assuming a 6.5% return, the present value is $863,159.06.

If an investor purchases the loan on September 30, 2026 for a price of $863,159.00 and holds the loan until all payments are made on time, they will earn an annual return of 6.5% on the investment. The total amount received will be $1,047,500.00.

Back to the Ultimate Financial Calculator.