Create a Schedule with Random Extra Principal Payments

To set your preferred currency and date format, click the “$ : MM/DD/YYYY” link in the lower right corner of any calculator.

A Step-by-Step Tutorial

Tutorial 9

Prepaying principal by making an extra loan payment reduces the total interest charges. It may also reduce the total number of payments. This tutorial shows how to calculate the effect of a one-time, random extra payment. Analyzing extra payments is one of the most frequently requested financial calculations.

All users should first complete the more detailed initial tutorial to understand the Ultimate Financial Calculator’s (UFC) basic concepts and settings.

To create a loan schedule with a random, extra principal payment, follow these steps:

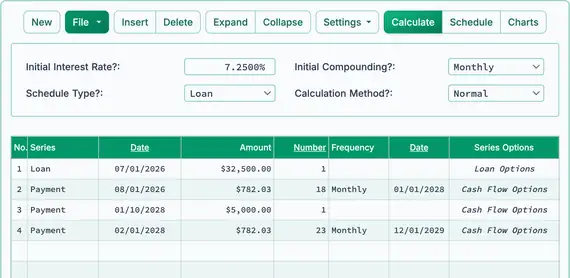

- Set Schedule Type to Loan.

- Alternatively, click to clear any existing entries.

- Click , then select Rounding Options. Set “Rounding” to Open balance — no adjustment.

- In the header section, apply the following settings:

- Select Normal for Calculation Method.

- Set Initial Compounding to Monthly.

- Enter 7.25 for Initial Interest Rate.

- In row 1 of the cash-flow input area, create a “Loan” series.

- Set the “Date” to July 1, 2026.

- Set the “Amount” to 32,500.00.

- Set the Number (of Periods) to 1.

- Note: Because the number of periods is 1, you will not be able to set a frequency. If a frequency is entered, it will be cleared when you exit the row.

- Move to the second row of the cash-flow input area. Select “Payment” for the “Series”. This example creates a schedule for a typical car loan with a four-year term. The regular payment amount is initially unknown.

- Set the “Date” to August 1, 2026.

- Set the “Amount” to “Unknown” by typing U. Fig. 1.

- Set Number (of Periods) to 48.

- Set the “Frequency” to Monthly.

- Click . The result is $782.03. Fig. 2.

- Click and make note of the interest due without an extra payment. Fig. 3.

- Next, prepare to enter the extra payment.

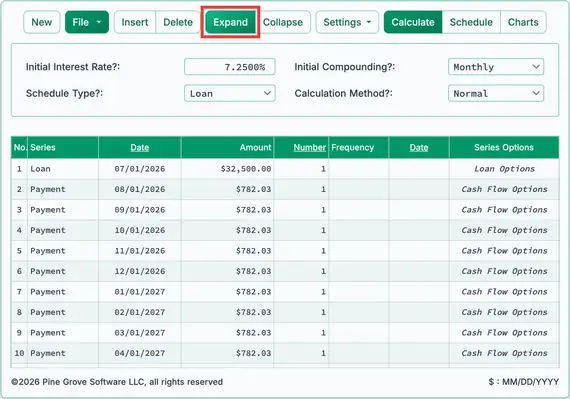

- Click on the button bar.

- automatically creates one payment per scheduled date. Fig. 4.

- There should now be 49 rows: one loan row and 48 payment rows.

- This creates space to insert the extra payment on the required date.

- You can also use the Expand feature to quickly create many payments. Each one can be edited individually for its date or amount.

- Click on the button bar.

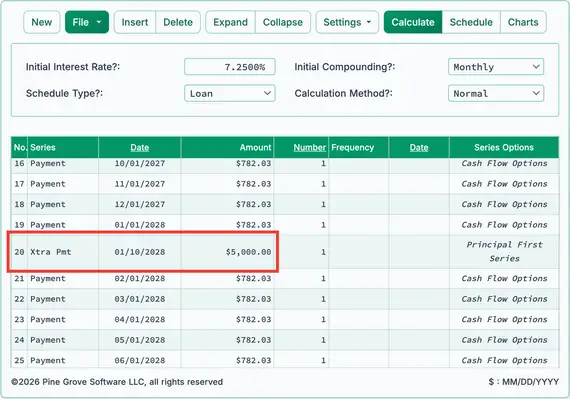

- Assume you receive a year-end bonus and want to make an extra principal payment on January 10, 2028. Click row 20. Row 20 will have a payment date of February 1, 2028. Insert a new row at this point:

- Click . A new payment row is created with a payment date of February 1, 2028 and a payment amount of 0.00.

- Change the date in this new row to January 10, 2028 (keep the amount as 0.00). Row 20 is selected so the extra payment is credited after the regular payment on January 1, 2026. When a row is inserted, it appears before the selected row—in this case, before February 1 and after January 1.

- Change the “Series” in the inserted row to “Xtra Pmt”.

- You may also insert a “Payment” instead of an “Xtra Pmt”. The difference is that “Payments” are applied first to interest due, while “Xtra Pmts” are applied directly to principal.

- Change the “Amount” to $5,000.00. Fig. 5.

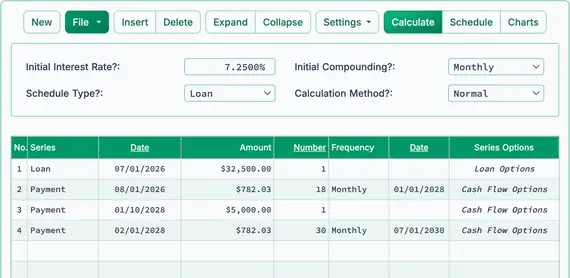

- Sort the payments by clicking on the button bar.

- You should now have a total of four rows: one loan row, 18 regular payment rows of $782.03, the extra-payment row, and 30 more regular payment rows. Fig. 6.

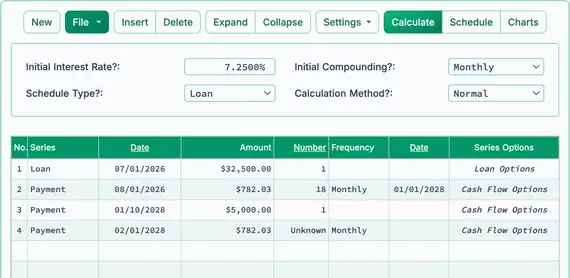

- Calculate the new term of the loan.

- The purpose of making an extra payment is to reduce interest. It also shortens the overall term of the loan. This step shows how the extra payment affects the schedule.

- In the fourth row, change Number (of Periods) for payments to “Unknown”. Fig. 7.

- Click .

- Due to the extra payment, the term is reduced from 48 periodic payments to 41 payments (18 + 23). Fig. 8.

- Click .

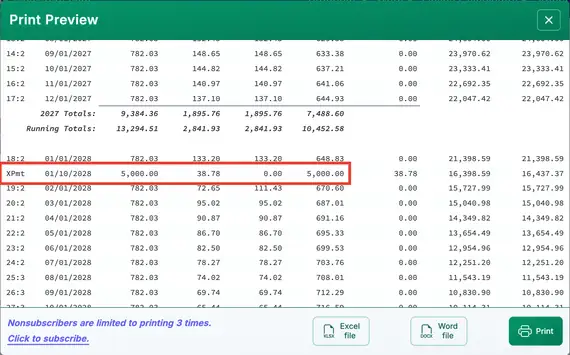

- Click to view a detailed amortization table showing the impact of the “extra payment” amount.

- The “Xpmt” entry reflects the $5,000.00 payment applied entirely to principal. Fig. 9.

- Any interest accrued up to the date of the extra payment (in this case, $38.78) is carried forward and will be collected with the next regular payment.

Screenshot taken from schedule printed to PDF.

- Observe the total interest paid when an extra payment is made: $4,178.54 vs. $5,037.30 (from Step 6), resulting in a savings of $858.76. Fig. 10.

- Because of the time value of money, extra payments have the greatest impact when made earlier or when the loan term is longer.

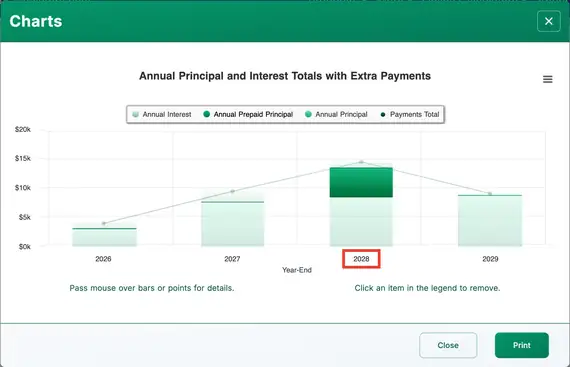

- To visualize the cash-flow stream, click . Fig. 11.

Note: An “extra principal payment” is not technically an “extra” payment. If the borrower owes the amount, then paying more toward principal along with a regular payment is not extra—it is simply paying part of the obligation early. The term “extra” applies only in the sense that the payment is not yet due. Therefore, a more accurate term is prepayment. Regardless of what you call them, the Ultimate Financial Calculator gives you full flexibility in deciding when to make them.

You may also apply the same method to enter multiple random extra principal payments. The ability to insert unscheduled payments into a cash-flow stream is what distinguishes the Ultimate Financial Calculator from other calculators on this site and elsewhere. This flexibility is why it can also serve as an auditor’s tool.

Back to the Ultimate Financial Calculator.